When Money Became Too Easy to Feel

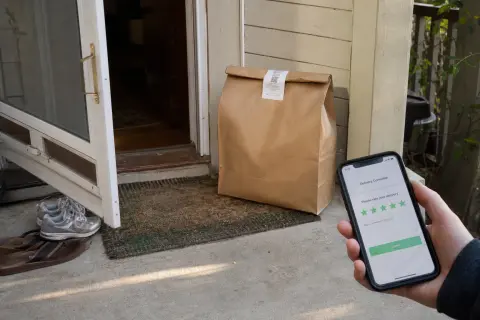

The first time Mara understood that money had gone quiet, she was standing in a grocery store at 8:43 on a Tuesday night, holding a carton of eggs and staring at a payment reminder for a shirt she barely remembered buying. The eggs were expensive, but not shocking. Nothing was shocking in public anymore. People just paused, looked at the shelf, and did the math in private.

Her phone buzzed again. Four payments remaining. A polite pastel notification from a buy now, pay later app. The shirt had cost less than dinner for two, which made the installment plan feel almost absurd at the time, the kind of financing meant for sofas or laptops, not a linen button-down from a summer sale. But there it was, waiting beside rent, utilities, ride-share charges, cloud storage, and the third payment on a vacuum cleaner that had seemed responsible because clean floors felt like evidence of control.

She put the eggs in her basket anyway.

At checkout, there was no belt, no cashier, no pause. She walked through a scanning gate with a receipt already forming in an app. The store took payment from her default card, which drew from an account she did not open often enough, which was buffered by a credit line she had promised herself she would only use for emergencies. The whole thing took less than three seconds. She missed, suddenly and with surprising force, the sound of coins.

Why did paying stop feeling like paying?

Not because coins were better. They were heavy, inconvenient, easy to lose. But they had weight before they became meaning. Bills folded and thinned out. Checks carried a ledger. Debit cards once required a little ceremony: swipe, sign, wait, hold the receipt, face the total. Even credit cards had friction. The clerk took the card. The machine coughed. The slip printed. There was time, however brief, to feel the transaction crossing from desire into consequence.

Now money passes like a shadow over glass.

For most of modern consumer life, payment was an event. It happened at the end of a purchase, in a place, under social conditions. You stood in line. You watched items move toward a scanner. You heard each beep. A total appeared, and even if you expected it, you had to meet it. People made jokes at the register when groceries ran high. They removed one item from the counter. They searched for coupons. The moment of payment was not only economic. It was emotional and public.

The old friction points

- Cash ran out, so spending hit reality early.

- Checks could bounce, which made the risk visible.

- Card readers and receipts created a pause.

- That pause gave people a chance to feel the cost.

Convenience changed the shape of the moment

First came cards that made cash feel old. Then online checkout reduced shopping to saved addresses and remembered numbers. Then mobile wallets turned a tap into a gesture so small it barely counted as a decision. Subscription billing normalized the idea that money would leave without participation. Delivery apps unbundled meals from kitchens, drivers from restaurants, tips from wages, and fees from awareness. Buy now, pay later removed the final pause between wanting and owning.

Each change made sense on its own. Nobody wants to type a card number every time. Nobody misses standing in a bank line to pay a bill. Nobody enjoys the embarrassment of a declined transaction. Convenience is not a trick invented in a boardroom. It answers real impatience, real fatigue, real friction in daily life.

What the culture keeps showing us

On TikTok, personal finance creators sort through app notifications and call it a debt audit, sometimes laughing, sometimes close to tears. Young workers share screenshots of bank accounts not as bragging but as confession. The phrase loud budgeting, popularized as a rejection of silent spending pressure, captures a mood that is less about thrift than self-defense.

At the same time, cash stuffing videos have become oddly soothing to watch. Rent. Groceries. Gas. Fun. Emergency. The appeal is not nostalgia exactly. It is visibility. The hand sees what the app hides. A person can watch a category empty out. The money has edges again.

The new anxiety is not the terror of one bill, but the mental load of many unfinished transactions.

What happens when small debts become emotional clutter?

Mara was not in crisis. This distinction mattered to her. She paid her rent. She had a salary from a design firm that made office software for teams that no longer had offices. She did not consider herself irresponsible. Her parents had carried credit card balances with higher interest rates and fewer tools. They would have considered her life sophisticated, perhaps enviable.

Still, she had begun waking up before her alarm with the sense that something was scheduled to happen. Not an emergency. Not danger exactly. A withdrawal.

Her calendar looked clean, but her money had appointments.

The invisible list

The amounts were usually small enough to ignore and frequent enough to create a hum.

Why are people accepting more control over spending?

The first sign that people wanted guardrails was not moral panic. It was exhaustion. Budgeting apps began to look less like spreadsheets and more like emotional infrastructure. Banks added spending insights that gently told customers when dining out was higher than usual. Fintech companies offered round-ups, lockboxes, payday advances, credit score coaching, subscription cancellation tools, and alerts that translated invisible movement into ordinary language.

But many people do not want more information. They already have too much information. What they want is a boundary that holds.

A boundary used to be built into the form of payment. Cash ran out. A check could bounce. A store closed at 9. A bank account could be checked only with effort. These boundaries were imperfect, sometimes punitive, and often hardest on the people with the least money. But they made spending encounter reality sooner.

A practical response

People deleted shopping apps after midnight. They put credit cards in drawers. They used prepaid cards for groceries. They created separate accounts for bills, food, travel, and guilt-free spending. They turned on transaction alerts not because they loved being notified, but because a buzz after every purchase restored a small moment of contact.

Households are adapting

Some couples share weekly spending summaries instead of shared accounts. Roommates use apps to settle utilities instantly, yet still fight because instant settlement does not solve uneven cash flow. Parents give teenagers debit cards with category restrictions and real-time alerts. College students are rediscovering cash for nights out because a stack of bills is harder to rationalize than a phone screen.

This is not nostalgia

Nobody wants to pay electric bills by mail forever. The shift is more interesting than that. People are trying to make digital money behave like something embodied. They want the intelligence of modern systems without the amnesia.

What might payment feel like in 2070?

By 2070, the payment moment may nearly vanish for many people, not because everything is free, but because spending has become embedded in personal systems that negotiate, approve, delay, and decline on our behalf.

Imagine a household where the primary financial interface is not a banking app but a domestic intelligence woven through appliances, transit, healthcare, school portals, and personal devices. It knows the household income rhythm, debt obligations, medical needs, food preferences, carbon allowances, insurance incentives, and long-term goals. The refrigerator does not simply order milk. It checks nutrition plans, local price fluctuations, household cash flow, delivery consolidation, and whether the family has exceeded its weekly convenience budget.

For the wealthy, this future may feel effortless. Bills will arrange themselves. Investments will rebalance. Travel will be reserved by agents that know not just preferences but mood patterns. Payment will be less an action than a background permission granted by abundance.

The split future

For everyone else, the same intelligence may feel like a gatekeeper. Spending will be classified, scored, timed. A system may say, not now. It may offer alternatives. Repair instead of replace. Wait three days. Choose the cooperative version. Use community credit. This does not fit your debt recovery plan.

In the best versions, these controls will be chosen and humane. In the worst versions, they will be imposed by lenders, insurers, employers, or governments, turning financial life into a permission architecture.

The future of payment may split along a quiet line: automation for those trusted by the system, restriction for those managed by it.

Can intelligent spending systems reduce anxiety?

They can, if they are designed around human realities rather than transaction volume. The best systems will understand that people do not only need to know whether they can afford something today. They need to know what today's yes will feel like next month.

They need payment timelines that gather instead of scatter. They need warnings that are neither shaming nor so gentle they become meaningless. They need a way to distinguish indulgence from sabotage, emergency from impulse, generosity from social pressure.

A humane system might translate a purchase into time. This jacket equals three lunches out, or two hours of work after taxes, or a delay in paying off the dental bill by nine days. Not as punishment, but as context. It might ask different questions depending on the hour. At 2 a.m., it might slow certain purchases. After a stressful calendar day, it might recognize vulnerability and suggest waiting until morning.

Before approving another installment plan, it might show all existing commitments on one plain screen, not hidden behind brand names and pastel progress bars.

The danger is that intelligence becomes paternalism. People already live under enough judgment. Low-income consumers are often over-monitored while high-income consumers are rewarded for the same behavior with points, lounges, and better credit terms. Any future system that claims to help must be accountable to the person using it, not merely to the institution profiting from their predictability.

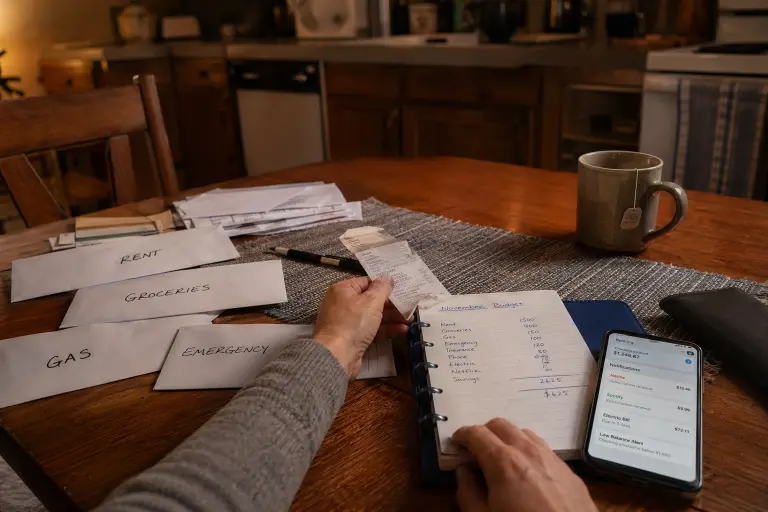

How Mara made money visible again

Mara eventually made a small ritual. Every Sunday evening, before the week began its usual grabbing, she made tea and opened every money app she had avoided. Not because she enjoyed it. She called it turning the lights on. She wrote the next two weeks of withdrawals on paper, in a notebook with a blue cover. Rent. Groceries. Installment. Insurance. Gift. Dentist. Shirt.

The first time she did it, she felt embarrassed by the shirt again. The second time, less so. By the fourth week, the notebook had become less a record of failure than a map of weather.

She canceled three subscriptions. She kept one she loved. She moved her grocery money to a separate card. She turned off one-click checkout on two shopping sites. She still used her phone to pay for the train. She still ordered takeout when she was tired. She did not become a different person. She became a person who could see the shape of her yes.

What this era seems to ask for

Not a return to inconvenience, and not a romance of scarcity. Just payment experiences that restore consequence without restoring shame. Money visible enough to respect. Flexible enough to serve. Slow enough, at the right moments, to let a human being catch up.

Common Questions About Easy Payments and Small Debts

Why do small digital payments feel less real than cash?

They often lack physical and emotional friction. There is no counting, handing over, waiting, or watching money leave. Because the action is reduced to a tap or automatic charge, the brain may register the convenience more strongly than the cost.

Are buy now, pay later services always harmful?

No. They can help people manage cash flow when used carefully and transparently. The risk comes when several installment plans overlap, making the true monthly obligation harder to see and easier to underestimate.

Why are subscriptions so easy to forget?

They are designed to continue without active attention. Their amounts are often small enough to avoid immediate concern, but over time they become part of a hidden financial baseline. Forgetting is not only a personal failure; it is part of the model.

What is a practical way to reconnect spending with reality?

Gather all upcoming payments into one visible place each week. Use a notebook, a calendar, or a budgeting app. The point is to see the timeline, not just the balance.